The 30% Mirage

Why the Permian Water Market Is Pricing Itself Wrong — And Who’s Quietly Buying the Other Side

“Be fearful when others are greedy, and greedy when others are fearful.” — Warren Buffett

Stand in a parking garage on a Tuesday mid-morning. Half the spaces are open, capacity is obvious. Stand in the same garage at 5:30 p.m. and you’ll see a different building. Cars circle, and drivers wait impatiently. The “available capacity” on the entrance sign is technically accurate but practically irrelevant.

This is the produced water market in the Permian Basin in 2026.

Total permitted injection capacity (via Salt Water Disposal Wells, SWDs – see other blog posts for reference) across the seven largest named midstream operators sits at 28.3 million barrels per day (BPD). Actual injection: 8.6 million, a blended utilization of roughly 30%.

If you were modeling the basin from a spreadsheet, you might conclude that produced water disposal is a sleepy, oversupplied corner of the oilfield. You would, of course, be wrong. And the operators who understand why are quietly buying the very thing the spreadsheet says is in surplus: capacity, optionality, and resilience.

The Number That Doesn’t Mean What It Says

Permitted capacity includes every SWD an operator has gotten regulatory approval to drill (active, approved-operational, and approved-but-not-yet-built). That last bucket is large. Across the named operators, 264 SWD permits sit in the pipeline today.

Those permits require capital to drill. The 30% utilization figure is measuring water moving through existing infrastructure against a capacity number that assumes every approved permit gets built.

Zoom into Loving County (the basin’s largest disposal market at 3.1 million BPD) and the disconnect grows. NGL runs at 26.8% reported volume utilization. WaterBridge at 25%. Plenty of headroom, the spreadsheet says.

The real constraint lies in the formation pressure data. Decades of high rate injection have increased formation pressure in injection receiving intervals and decreased the ability to inject fluid below regulatory limits.

NGL’s average dynamic bottomhole pressure in Loving County is 4,552 PSIG (the highest in the Permian). Its pressure utilization, the ratio of injection-state pressure to the formation’s resting state, is 134.6%. Between January 2024 and January 2026, NGL’s injection efficiency in Loving (barrels disposed per PSI of wellhead pressure) collapsed from 2,557 to 1,315 BPD/PSI. Roughly twice the surface pressure now produces the same volume in the ground. This is what capacity exhaustion looks like.

Dan Yergin has been making a point lately that translates directly here. Markets price energy on cost. Countries make energy decisions on security. When systems become fragile, optionality reprices upward. The lowest-cost molecule isn’t always the most valuable — the question is whether it’s deliverable when the system is under stress.

Substitute “molecule” with “barrel of disposal capacity” and you have the frame for what the smart operators in this dataset are doing. They are paying for resilience: multiple basins, multiple counties, multiple disposal intervals, pressure-aware infrastructure, and permit optionality in markets they have not yet entered.

The market is still pricing this business on cost per barrel and headline utilization. The operators are pricing it on optionality. That gap is the trade.

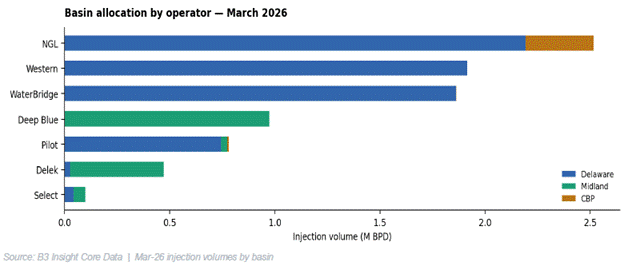

Seven Operators, Seven Postures

NGL leads the basin at 2.52 million BPD. Its 16 pending wells in Loving are a direct response to the capacity deterioration its existing wells are showing.

WaterBridge has the strongest growth at 22.1%, the largest permit pipeline in the basin (74 wells), and a strategy of running more wells at lower per-well intensity. Its dynamic-static spread in Loving has remained roughly flat while NGL’s has nearly doubled. It is also buying optionality in the Central Basin Platform with 29 approved permits in Andrews County, where it currently has zero injection volume.

Western carries the most constrained headroom in the dataset (0.40 average, 0.16 in Lea County) and Loving injection efficiency down 67%. The 21 pending permits it holds in counties where it has no current production (Gaines, Andrews) are exactly the kind of optionality purchase Yergin describes.

Deep Blue is the Midland counter-narrative: 96% share in Martin, 30.9% growth, lower-pressure formations, 15 pending wells in its anchor county. The cleanest growth story in the dataset, with a 0.30 headroom score in Howard County as the asterisk.

Pilot is the pure diversification play, twelve counties, 35 wells in the pipeline across six markets, the highest headroom scores among Delaware operators. No dominant position anywhere, by design.

Why This Matters for Capital

Three observations for anyone underwriting exposure:

• The relevant capacity metric is not permitted BPD. It is the dynamic-static spread, the injection efficiency trend, and the static BHP trajectory at the formation level. These diverge from headline utilization in exactly the counties that matter most.

• Permit pipelines telegraph CapEx commitments months or years before they show up in operating metrics. Reading the pipeline tells you where capital is going before it gets there.

• The disparity in scale, headroom, and optionality is wide enough that consolidation pressure is structural rather than cyclical. Resilience trades at a premium in constrained systems. The operators who built it early will be paid for it. The ones who didn’t will be the acquisition currency.

Greedy When Others Are Fearful

The Permian water midstream business looks oversupplied, but it is not. It looks low-growth, but it is structurally constrained. It looks operationally undifferentiated, but read the spread data and you can tell the operators apart with high resolution.

This is the setup Buffett was describing, a market the consensus reads one way while the data reads another. The operators paying for optionality today are the ones who will price it back to the market tomorrow. The 30% number is a mirage. The resilience premium is real, and it is just starting to get priced.

The full B3 Insight Permian Water Midstream Report covers seven named operators across all Permian counties — pressure trend data, permit pipeline detail, headroom scoring methodology, full competitive positioning. Available for institutional use. For more information please email info@b3insight.com